How many CDR registries will there be?

A reflection on CDR.fyi's (excellent) mapping of CDR-Registry-Protocols dynamic

A recent post from CDR.fyi had me thinking about the growth in CDR registries and protocols as the industry itself grows. In particular, what happens to the registries as marketplaces? At the moment there are around seven major registries with ~35 protocols across eight CDR methodologies. Registries Isometric, Verra, and Puro are among the busiest registries compiling protocols [edited with reader feedback - had ‘P’ capitalized which made it seem like ‘Proprietary’ was a registry rather than individual supplier protocols that are … ahem, ‘proprietary’ - thanks Nick for the DM - definitely not a source material problem, but rather a thinking out loud problem on my part].

Consolidation seems likely if the market participants (buyers and sellers of carbon removals) prefer standardization and interoperability, which would reduce transaction costs and complexity in their procurement processes. This seems likely - Microsoft will prefer one registry to satisfy their CDR purchases, and suppliers would prefer to list on one marketplaces according to one standard (or protocol). As certain registries gain a reputation for reliability and stringent standards, smaller or less efficient registries might merge or be absorbed by larger ones. This could be driven by the need for better recognition and trust from global markets and policy frameworks as CDR MRV and purchase behavior matures. I think this is probably also even more likely as more types of buyers enter into the market there will be pressure to consolidate underpinned by the pressure to standardize onboarding processes.

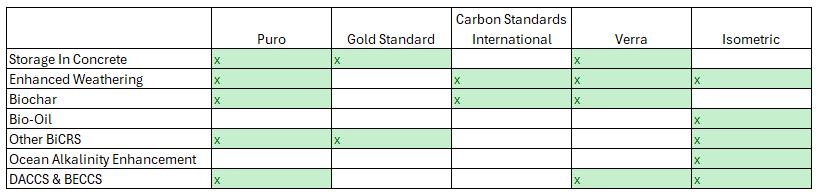

[Updated w/ reader comments] Looking at the overlap in registries, there seems opportunity for alignment in protocols regarding enhanced weathering (4), storage in concrete (3), biochar (3), other BiCRS (3), and DACCS/BECCS (3). This also seems to motivate me to dig in a bit more OAE and bio-oil being relatively less-defined in the registries to date (though that’s bound to change). (Noting here Isometric’s OAE is in public consultation). Welcome notes on this as still working my way through materials.

That said, diversity in registries might persist if different technologies for carbon removal need specialized validation approaches or if regional differences necessitate distinct standards and verifications. Moreover, niche markets may develop that focus on specific types of carbon removal, supporting the existence of multiple registries. Based on the expansion plays of registries like Isometric, clearly the registries don’t seem to think this is likely - staffing up quickly and outputting protocols faster than Deep Sky announces partnerships.

Regulation will play a role in the standardization and potential consolidation of the CDR registry market. Regulatory developments, such as international agreements on climate action, could drive standardization across registries. If strict guidelines are established globally, registries will need to conform, potentially leading to a more homogeneous market with fewer, more robust players.

Technology is also a driving force of potential consolidation - especially in MRV data layers and hardtech across CDR subtypes - might also influence the number of registries. As MRV matures, becomes more advanced and streamlines the verification process, this is likely to end up with a ‘winner take all’ outcome (biggest grouping of buyers and sellers edge out smaller registries, with little differentiation other than critical mass of the marketplaces creating network effects within).

Quality v. quantity - registries protocols are essentially working to standardize the quality of the product on offer (i.e., the CDR). So to some extent there is a quality battle happening between registries - and risk one of them falls down with stories of poor quality processes by one of their suppliers sneaking through. But more likely in my mind is this is a ‘get there first’ race to onboard as many buyers and sellers as possible, whilst keeping quality in check. That - and the behavior of the registries themselves - seems to suggest to me it’s a theme battle (i.e., publish protocol on biochar, race to onboaord suppliers, attract sellers, move to next CDR method).

Any marketplace specialists out there - or people more familiar with the protocols themselves (especially on biochar, concrete, and alkalinity enhancement where there is overlap between registries) - I welcome comments and input on where you think this goes in the medium-term. Definitely still learning and always curious.