Could import regulation shift the landscape of CDR credit buyers?

Question series (thinking through CCDR out loud)

Who buys carbon removal credits? This has come up a few times recently for me in conversations - with early stage CDR tech developers looking to understand their commercial route and customer. There’s a held view that carbon removal credits are bought by big tech firms but that outside of that there’s not really a customer base.

Frontier (Stripe, Alphabet, Shopify, Meta, McKinsey), Google, and Microsoft are leading in commitments to buy carbon removal credits. It's unsurprising that this is the perspective suppliers have. I’d like to suggest there is another, more traditional buyer out there for carbon removal credits: manufacturers. Specifically, manufacturers exporting to Europe and the UK.

The current state of CDR purchases

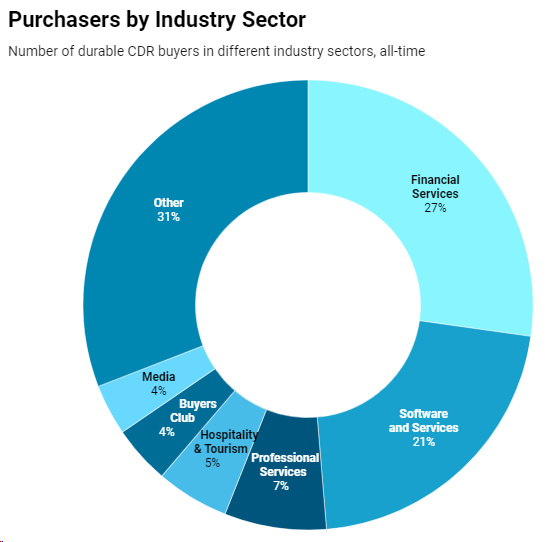

The Carbon Dioxide Removal (CDR) market has witnessed explosive growth, with purchases increasing 7.3x to 4.5 megatonnes in 2023 from 0.615 megatonnes in 2022. This growth is driven by large deals involving ‘big tech’ buyers such as Ørsted-Microsoft and Heirloom-Microsoft. As per the (excellent) CDR.FYI annual report, primary sectors purchasing Carbon Dioxide Removal (CDR) include Financial Services (27%), Software & Services (21%), Professional Services (7%), Hospitality & Tourism (5%), Buyers Clubs and Marketplaces (4%), and Media (4%).

How a carbon price for imports might incentivize new CDR buyers

Whilst it’s been true that large tech (and consulting firms) have driven most of the commitments for CDR credits, moving forward companies selling physical goods to Europe and the UK have an incentive to buy CDR credits. Why? Well, to help them decarbonize their value chains and access markets increasingly levying against the carbon footprint of goods.

In the EU, the European Carbon Border Adjustment Mechanism (CBAM) entered into force in October 2023 and can be expected to work through imports to affect overseas manufacturers behavior in the next few years. The UK’s version of this - also CABM - will come into effect by 2027 and as with the EU model will ensure imports of iron, steel, aluminum, ceramics and cement from overseas will face a comparable ‘carbon price’ to those goods produced in the UK. For the sake of this post, I’m going to assume that the UK approach to CBAM doesn’t fall far from the EU’s model…

The CBAMs are designed to encourage cleaner industrial production outside the EU & UK by putting a fair price on the carbon emitted during the production of goods entering the EU & UK markets. Exporters to these markets will face a financial incentive to reduce their carbon footprint to avoid the added costs associated with the CBAMs. This could lead to increased investment in carbon removal technologies and services, such as DAC, to mitigate emissions more cost-effectively.

Manufacturers in those exporting countries that can demonstrate lower carbon emissions for their products would find themselves at a competitive advantage under the CBAMs. This is likely to increase the demand for carbon removal solutions from manufacturers of iron, steel, aluminum, ceramics and cement products in places like India, Vietnam, Malaysia, UAE etc. that are exporting to Europe and the UK. These companies will face either a CBAM charge for unabated emissions or up to that amount for decarbonizing their value chain (including by CCUS and CDR methods).

During the transitional phase of CBAM, importers of these types of goods will need to report greenhouse gas emissions embedded in their imports, although financial payments or adjustments based on these reports will only start from 2026 in Europe. This requirement for detailed emissions reporting will likely spur demand for carbon accounting and removal services to ensure compliance and optimize the reporting process.

So what?

I see two potential effects for carbon removal from CBAM: first, stimulating CDR demand from exporters; second, stimulating the investment into MRV solutions to support the carbon accounting of imports.

What could that mean in practice? Countries and companies who are reliant on exports to the EU (and the UK) might explore strategic partnerships with existing DAC companies and other quality carbon removal ventures to meet CBAM requirements more effectively. These collaborations could include investments in local carbon removal projects or long-term purchase agreements for carbon credits. I haven’t seen this yet (let me know in the comments if you’ve come across any cases like this).

I also expect to see established CCUS, DAC & CDR companies start to branch out and locate sites in exporting countries or partner with local implementers. For example, India’s Oil and Natural Gas Corporation (ONGC), a government-owned oil and gas explorer and producer, recently signed a MoU with Norway-based energy company Equinor to explore opportunities in CCUS projects.

I would predict that you’ll start seeing homegrown DAC & CDR ventures in exporting countries. This is especially true of DAC (and CCUS) when sites can be co-located with manufacturing facilities to benefit from engineering talent. I haven’t seen too much evidence of this yet (other than Octavia Carbon), but based on conversations I’ve had with early stage founders - in India, SE Asia - I think we’ll start to see traction in this space (especially for DAC where technology moves from novel to off-the-shelf for developers).

I would also expect to see emerging market governments with natural advantages in the form of cheap power & (relatively) cheaper engineering talent (e.g., Kenya, India, Indonesia) to set up regional ‘hubs’ for CCUS, DAC, and geological storage - probably colocated with oil and gas production, if not yet colocated with manufacturing. DAC will piggy-back off of CCUS tech advancement (skills, downstream/upstream infrastructure and supply chains). These have already started to be seen in Iceland and the US, and make sense to co-locate engineering talent, upstream and downstream/offtaker infrastructure - and even conceptually build a ‘critical mass’ around the suppliers. It’s also just a shape of solution governments are familiar with - special economic zones (SEZs) being typical approaches to developing manufacturing bases in these markets. An example from emerging markets would be the Indonesian government's new guidance encouraging oil and gas companies to install CCUS alongside their facilities.

What about nature?

Yeah, I agree. “If all you have is a hammer, everything looks like a nail”. That’s us with industrial technology. We can co-locate a DAC facility to a ‘hard-to-abate’ emitter (aluminum & steel manufacturing, cement, etc.). A contact of mine recently asked me ‘at what distance from an emitter can a CCUS be considered a DAC?’ It’s a tongue in cheek question, but gets at the problem: we’re so used to solving with technology that we see rebalancing the carbon cycle as an industrial-technological challenge.

But! It brings me back to my first two predictions that will come out of the CBAM working through imports: (1) stimulating demand for DAC and CCUS…, but also (2) investment in MRV to improve carbon accounting across the value chain.

My feeling is as (2) happens, as we get better able to measure, verify, and report durable and quality carbon removals, buyers and investors will move beyond DAC (where it's easy to see at least investor attention currently sits) and towards more nature based solutions. I’m particularly bullish on soil accrual (because it’s a triple win), enhanced weathering (because it’s material handling, which we’re really good at…), and OEC & other mCDR (in particular pelagic macroalgae, but that’s a blog for another time!).

So for now, just to say that as import restrictions in Europe, the UK … maybe the US (?) that try to price carbon into goods come into effect this will incentivize exporters on the other side to invest or partner with CDR, DAC, and CCUS technology providers - and that as MRV matures, we can hope this demand will spread to nature-based systems which aren’t as easily co-located with emitters.